When listing the world’s businesses by revenue, the ‘big tech’ concerns like Meta, Alphabet and Amazon will appear at, or near, the top. Each has a strong market presence. Most people use their products. Naturally, they attract attention.

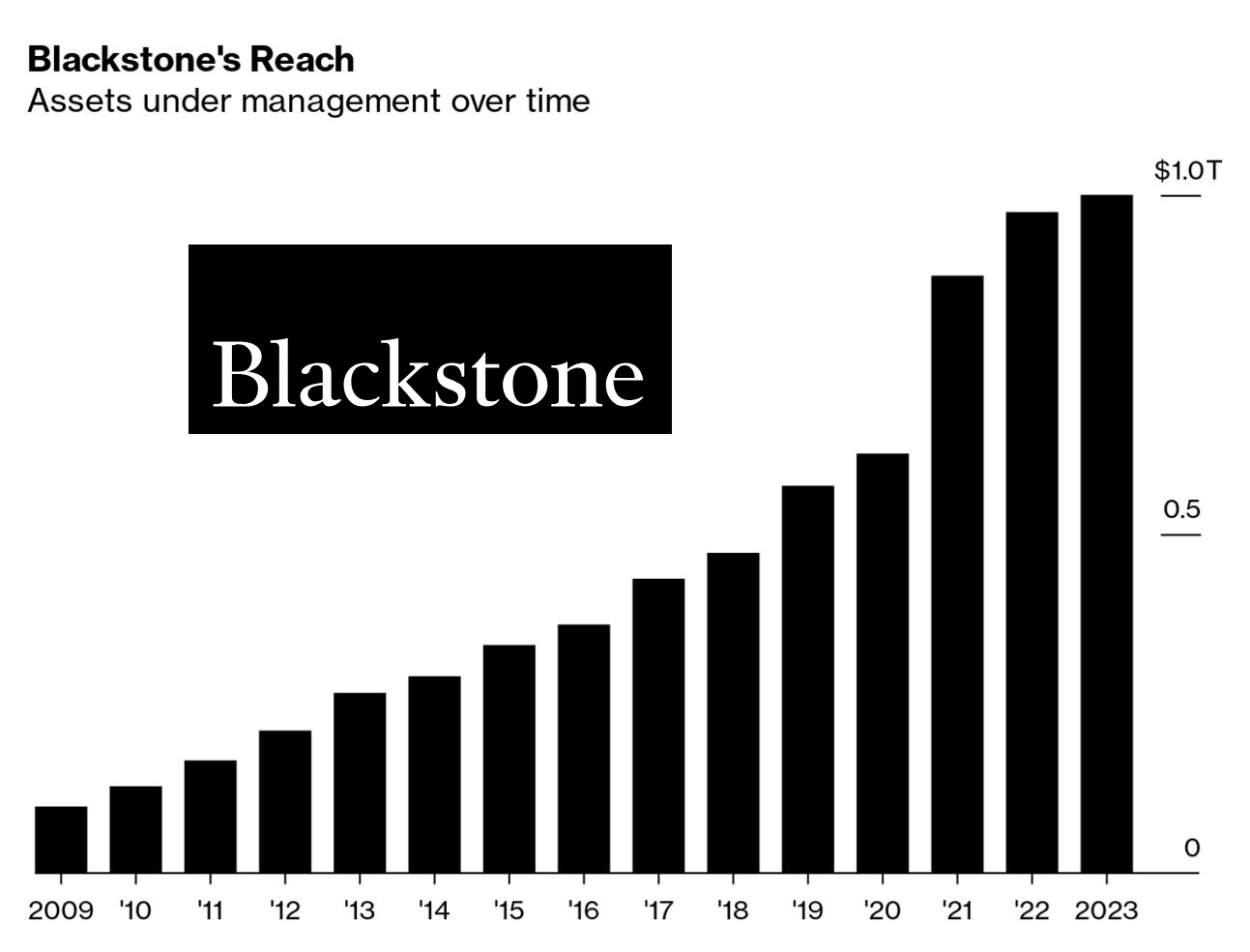

But in terms of sheer financial power, private equity firms can eclipse even the tech giants. The Blackstone Group is the world’s largest private equity firm. While Apple (the world’s largest technology company by revenue) controls $352 billion in assets, Blackstone manages over $1 trillion, roughly triple Apple’s holdings.

Blackstone’s expanding reach: Assets Under Management from 2009 to 2023, nearing the $1 trillion mark. (Source: Bloomberg.)

Unlike Apple, Blackstone’s influence isn’t on consumers. Like most private equity firms, it functions by buying, restructuring, and selling businesses for profit. Critics of the model point to the disastrous effects on these acquired businesses and their workers.Fewer industries are as opaque. The extent to which private equity firms conceal their affiliates, structures and day-to-day operations is disconcerting. When Blackstone chairman Stephen Schwarzman hosted an extravagant birthday party, other private equity firm owners criticised him for the media coverage the party brought with it.

Blackstone CEO Stephen Schwarzman and his wife invite guests to an extravagant birthday celebration at his luxurious Miramar estate.

From Obscurity to Economic Dominance: The Rise of Private Equity

The earliest private equity firms arose in the early and mid-20th century. In the 1980s, at least one private equity firm made the cover of Time magazine, a marker of the extent to which the industry had impressed itself on the Anglosphere. At the time, fewer than 1,000 private equity firms existed worldwide.

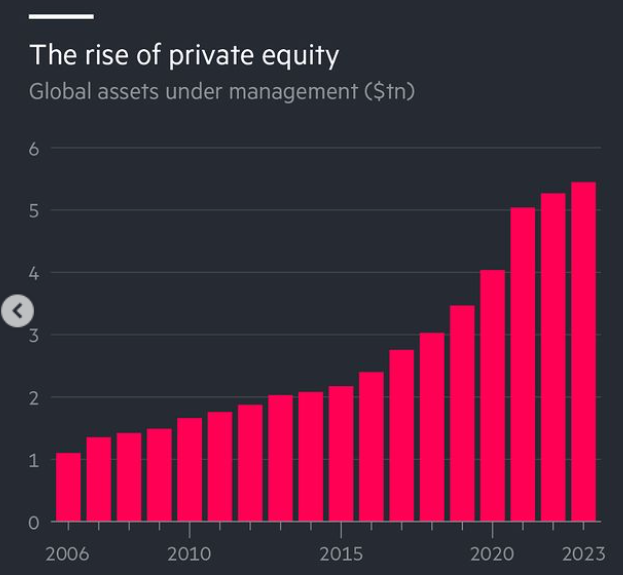

The rise of private equity: Global assets under management have grown significantly, reaching over $5 trillion by 2023. (Source: Financial Times.)

Today, there are more than 15,000 in the United States alone, where they control tens of trillions of dollars. They are no longer specialised segments of the economy but dominant enterprises that can control whole nations.

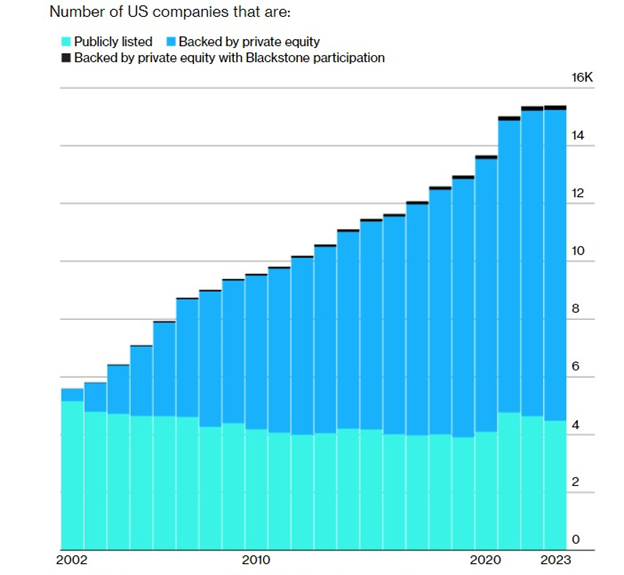

Growth in the number of U.S. companies backed by private equity, 2002–2023. Companies with private equity backing, including those with Blackstone participation, have increased significantly, overtaking publicly listed companies.

How Private Equity Works

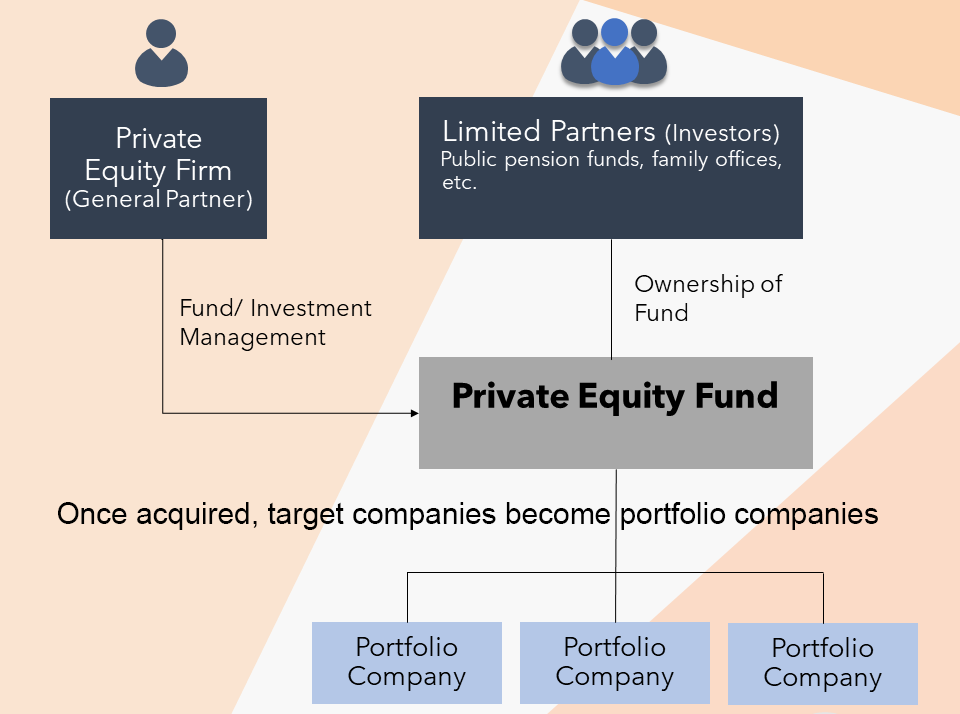

Private equity firms raise large sums from institutional investors like retirement plans, university endowments, non-profits, wealthy families, and individuals. They pool this capital into funds. (Because high finance and private equity often couch their processes in deliberately obscurantist jargon, it is necessary to define some further terms for clarity.)

The institutional investors are known as ‘limited partners’ (LPs) because they have limited control over the fund’s operations; they provide the capital but do not make management decisions. The private equity firm acts as the ‘general partner’ (GP), managing the fund, charging investors management fees and making investment decisions. They borrow additional capital from banks to maximise buying power. (The next section expands on the role borrowed money plays in private equity takeovers.)

Once the fund is established, the firm begins buying ‘target companies’, usually businesses in distress. After acquisition, these companies are known as ‘acquired companies’, or ‘portfolio companies’ and become part of the firm’s collection of investments.

A simple structure of a private equity fund showing investors (limited partners), the private equity firm (general partner) and portfolio companies.

The goal is to increase the value of these companies, then sell them at a profit, a process known as an ‘exit strategy’. Most private equity firms hold acquired companies for about 3 to 5 years before selling. Profits from these sales are split between the investors and the private equity firms.

Leveraged Buyouts: The Essential Private Equity Play

Private equity firms developed and perfected the leveraged buyout (LBO), transforming it into their primary weapon of wealth extraction. The term comes from a private equity firm’s use of leverage (borrowed money) to cover part of the cost of acquiring a target company. Loaned money is used in addition to fund capital. The rub? The acquired company, rather than the private equity firm, is responsible for repaying these loans.

An analogy may be helpful: Paul buys Alan’s car using Alan’s credit card. Paul either repairs and sells the car or strips it for parts. Paul keeps the profits and then returns the credit card to Alan, telling him to pay off the debt.

The analogy is simple and not fully explanatory, but a useful way to demonstrate how LBOs work.

Paul represents the private equity firm; the car is the acquired company, and Alan is the acquired company’s owner and the stakeholders who bear the debt burden. The credit card represents the lender money private equity firms use (along with investor cash) during LBOs.

Basic structure of a private equity-backed leveraged buyout (LBO): PE Fund is the private equity fund (the fund managed on behalf of institutional investors). Banks loan money to help finance the acquisition, and the acquired company must repay these loans.

Acquired companies are expected to continue trading, amplify their revenue, and do all this while paying off debt and interest the private equity company has transferred to their balance sheets. It is a process that can tip a troubled firm into greater distress. It explains why so many private equity-backed companies default after they’ve been purchased.

The House Always Wins: More Methods of Harvesting Money

Because they hold so many poorly-rated, distressed companies, they want to get rid of them as quickly as possible. So, private equity firms are necessarily short-term operators. Short-term profiteering is the cornerstone of the private equity industry.

Private equity firms can make loan sharks look altruistic. Ethical concepts like beneficence are absent from the private equity world. Exceptional penny-pinchers, they’re constantly finding new methods to make money. Profit is king. The focus is fast profits at minimal expense. Long-term operational recovery is the remit of others. LBOs are just the beginning.

After acquisition, private equity firms deploy diverse methods to extract wealth. Within months, they’ll cut or replace management. That achieved, they can force the acquired company to cut costs, fire employees, strip off and sell assets, or even take on usurious loans. They can compel acquired companies to use services from private equity affiliates, creating another profit stream.

If they retain the original board, they charge hefty management and consultancy fees. Private equity firms may also require the acquired company to buy other companies in a strategy known as a ‘platform acquisition’ or ‘roll-up’. In a roll-up, a private equity fund first buys a primary company (a ‘platform’) and then directs it to acquire smaller, related businesses (‘add-ons’) to expand its market share and attractiveness to buyers.

In doing so, the private equity firm effectively transforms the platform company into a private-equity proxy, using it as a vehicle for further expansion and profit extraction.

Structure of a platform acquisition with add-on companies.

Should default loom, they’ll pick portfolio companies apart, selling off everything from property to workwear.

So are private equity firms pioneers, predators, or both? They’re both.

Actions, Words and Warnings

Assured Trade believes in commerce as a force for good. Private equity firms repeatedly operate against this principle, both in action and by reputation. When private equity billionaires like Texan David Bonderman, the co-founder of TPG Capital, say things like, “a good default, like Portugal or Greece, would be very good for the private equity business”, they reveal the exploitative mindset of their board members.

Warren Buffett, founder of Berkshire Hathaway and investment virtuoso, has criticised private equity firms, calling them “dishonest” for excessive management fees and self-serving practices. “If I were running a pension fund,” Buffett has said, “I would be very careful about what was being offered to me.” He’s warned that “when trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients.”

Warren Buffett’s critical view on private equity as quoted, with major firms pictured.

Statistician and former trader Nassim Nicholas Taleb claims that “private equity has absolutely no reason to exist. The private equity holder has all the upside and the banks all the downside.” Profits flow to private equity firms while the financial burdens are shifted to acquired companies and lenders. It is an imbalance of risk and reward.

A Growing Reach: From Prisons to Water Rights

Private equity’s reach extends into every area of commercial activity. Firms like CoreCivic and GEO Group have slashed costs and staff in America’s private prisons. With gang intelligence units eliminated, prison gangs flourish. Infrastructure crumbles. Conditions mirror the Dark Ages but with modern levels of violence and disease.

No trespassing sign outside a CoreCivic-owned prison in Arizona. CoreCivic has received investment from various private equity firms over its history and continues to attract institutional investment, including from private equity sources, seeking returns from its extensive network of detention facilities. (Source: Reuters.)

In pharmaceuticals, private equity-acquired companies like Vyera and Valeant raised prices while cutting research and development. Security breaches expose confidential information as private equity firms acquire data analytics and AI startups.

Even basic human necessities aren’t safe. Private equity firms now target water rights and facilities, marketing access to resources necessary for continued human existence.

The Shadow Network: Sovereign Wealth Funds and Private Equity Firms

The relationship between private equity firms and sovereign wealth funds (huge state-owned investment vehicles managing national savings) shows another dark aspect of the industry. Through layers of subsidiaries, shell companies, and complex financial structures, private equity firms broker deals that transfer control of crucial services and resources to foreign state actors. These arrangements occur through networks so circuitous that traditional concepts of national ownership become meaningless. Shadowy meshes of deals and counter-deals are all designed to disguise ownership and control.

If there exists a method to generate profit by skirting regulatory oversight, private equity firms have thought of it. They’ve implemented it, are implementing it or will implement it.

They’re innovators who don’t create value but discover new ways to gain hold of it, whether through complex financial engineering or murky ownership formats that blur the lines between private capital and state control.

High Risks, High Stakes

Private equity has an allure for institutional investors. It offers them the chance to make higher profits than they would with conventional investments like cash, bonds or shares, especially when interest rates are low. But high rewards mean, in the private equity sector, high risks. When junk-rated assets collapse or underperform, investor returns diminish.

Banks, too, face risks when lending to private equity-backed companies, especially if acquired companies default. The potential exists for the destabilisation of entire financial systems.

Low interest rates have historically benefited private equity firms, allowing them to borrow cheaply for acquisitions. When rates rise, their debt-laden companies struggle, and investor returns diminish.

In periods when interest rates are high, private equity firms place additional debt onto acquired companies, pushing them toward bankruptcy while using unscrupulous accounting to make the companies appear more creditworthy.

Deaths, Starvation, Defaults and Job Losses

Private equity firms have destroyed companies in every sector.

One in every 20 American nursing care facilities is owned by a private equity firm. The problems with a short-term focus on profitability in this area, where cutbacks can cause deaths, should be obvious. Private equity-owned nursing homes reported higher mortality rates and worse conditions, with cost-cutting measures reducing staff and quality of care.

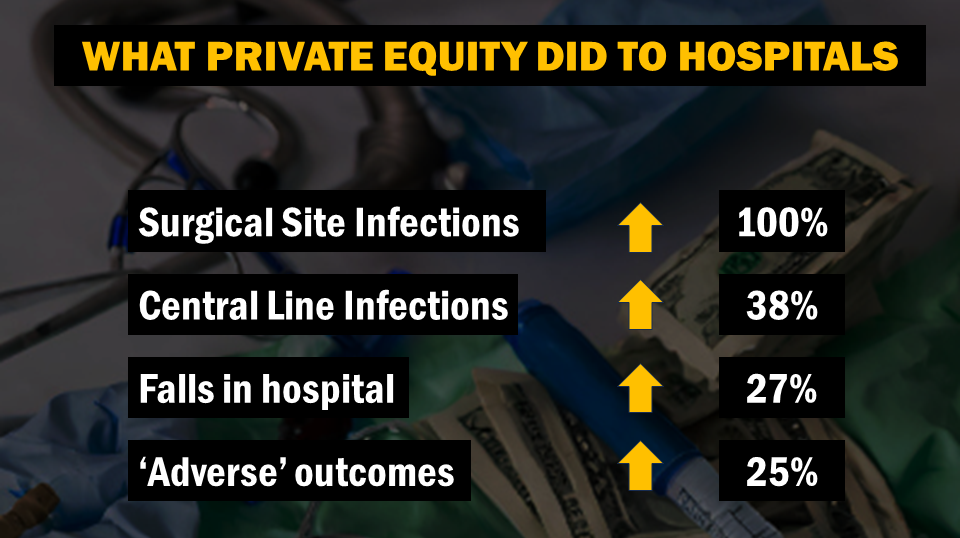

Early private equity firms had no presence in healthcare. By the 2000s, they recognised the profitability of American government-funded programs like Medicare and Medicaid. By the 2010s, private equity investments in hospitals accelerated and continue to do so. Today, a third of all for-profit hospitals in the United States are owned by private equity firms. Studies show that hospitals acquired by private equity firms have compromised care, reduced resources, and increased incidents of adverse events. Falls and infections increased by 25% when private equity firms took over hospitals in 2023. Costs inevitably went up. Such hospitals serve vulnerable rural communities, where reductions and closures can render healthcare inaccessible.

Increases in adverse hospital outcomes following private equity acquisition. (Source: Kannan et al, JAMA, 2023.)

Private equity firms are notorious for obliterating retail companies. The big UK supermarket firm Debenhams and the toy maker Toys R Us were both acquired by private equity firms, and their balance sheets were loaded with debt. Both ended up filing for bankruptcy. When Debenhams, one of the UK’s oldest businesses, shut its doors, 25,000 people lost their jobs. The closure of Toys R Us forced 33,000 people to find new work.

Closed Toys ‘R’ Us store with ‘For Lease’ sign. (Source: LA Times.)

In 2018, car parts manufacturer Wheel Pros, which had served 30,000 retailer firms worldwide, was acquired by Clearlake Capital. The private equity firm used a ‘roll up’, forcing Wheel Pros to buy the automotive lifestyle brand Hoonigan. Clearlake merged the two firms and encouraged Wheel Pros/Hoonigan to acquire over 40 other companies and brands. The approach imposed $1.75 billion in debt on Wheel Pros/Hoonigan, which filed for bankruptcy in September 2024.

Private Equity’s Defence and the Statistical Realities

Supporters of private equity argue that these firms inject capital into struggling businesses, helping them grow. Proponents claim that private equity expertise allows these companies to expand faster, enter new markets, and operate more efficiently.

Critics say this apparent efficiency means layoffs, reduced quality and asset sales. For struggling companies, the added debt from a leveraged buyout can mean a slide toward collapse rather than recovery.

A recent Moody’s analysis of fast-growing American private equity firms is edifying. From January 2022 to August 2024, private equity-backed companies defaulted at 17% —double the rate of independent companies. The most aggressive private equity firms drove acquired companies to bankruptcy. Nearly a quarter of Apollo Global’s acquisitions defaulted between 2022 and 2024. Almost half of Ares Management’s portfolio companies are in distress. Companies owned by Clearlake Capital – including Chelsea FC – face mounting pressure from rising rates, spotlighting the dangers of debt-heavy acquisitions.

The Way Forward: Amending Private Equity

Not all private equity firms are destructive. Although firms of this sort are abnormal, they do exist. Acting in the interest of portfolio companies, they avoid LBOs, create long-term value, aid growth and do this in a careful, considered way. They’ll help distressed companies by renegotiating prior loan obligations, giving the companies time to stabilise and improving cash flow and cash reserves. It is lamentable that they’re exceptions, but it is important to recognise their existence and praise their conduct. They’ve demonstrated the ability to help their investors, themselves and the companies they own. Open and scrutable, they make profits because they are prudent. These firms show a better path ahead.

Still, they’re outliers. In private equity takeovers, LBOs are the norm. Corrosive practices which undermine acquired companies are conventional.

Reform requires more scrutiny and accountability. Private equity firms must open their books, revealing management fees and operational details. Those that operate responsibly deserve recognition, potentially encouraging others to follow suit. Better disclosure can help reduce harm.

At its best, commerce creates value, builds communities, and drives innovation. Trade, when conducted with integrity, benefits all participants. Yet private equity’s usual tactics too often corrupt these principles, replacing genuine value creation with value extraction.

If commerce is to retain its role as an engine of prosperity, private equity must evolve beyond predation and short-term profits. Unchecked, private equity’s influence will continue to grow, taking a toll on people and businesses. It will leave a trail of stripped assets, broken companies and wrecked economies behind it, with more of the same ahead.